ASI Webinar

Learn about our expansion initiative CUChoice. This initiative aims to amend the Michigan State Credit Union Act to give state-chartered credit unions the option to choose between private or federal deposit insurance.

Innovative Deposit Solutions

through ASI since 1974

Greater Coverage

$250K PER ACCOUNT

ASI’s primary insurance offers $250K of coverage per account, not per individual, with no limit to the number of accounts held by a member.

Greater Peace of Mind

ABOVE & BEYOND

Excess share insurance is a credit union exclusive program. Protect your members with deposit coverage up to $5 million on top of your primary insurance coverage.

Greater Stability

SINGULAR FOCUS

For 50 years, ASI has protected the deposits of our credit union members. No member has ever lost money in an ASI-insured account.

Gain a Competitive Edge

Member Success Story

“Without private share insurance through ASI, Abbott Laboratories Employees Credit Union (ALEC) would not exist. ASI helped us establish ALEC in 1990 and provided private deposit insurance protection when no other organization could. Today we stand 31K members strong and with more than $1 billion in assets. Over my 20+ years at ALEC, I’ve seen how private insurance can be a game changer for credit unions!”

“Without private share insurance through ASI, Abbott Laboratories Employees Credit Union (ALEC) would not exist. ASI helped us establish ALEC in 1990 and provided private deposit insurance protection when no other organization could. Today we stand 31K members strong and with more than $1 billion in assets. Over my 20+ years at ALEC, I’ve seen how private insurance can be a game changer for credit unions!”

— Joseph Trosclair, President/CEO of ALEC

The Numbers

1.35 Mil+

members protected through ASI’s primary coverage

$19 Bil +

of members’ deposits protected

$250K+

in per account coverage, not per member

Your Members Own Your Credit Union

Our Members Own ASI

Just like your credit union, ASI is owned by the members we serve. As such, our primary mission is to see our member credit unions grow and prosper. Our board of directors is elected by our members, and our member credit unions have a voice in the strategic direction of the program.

Featured Items

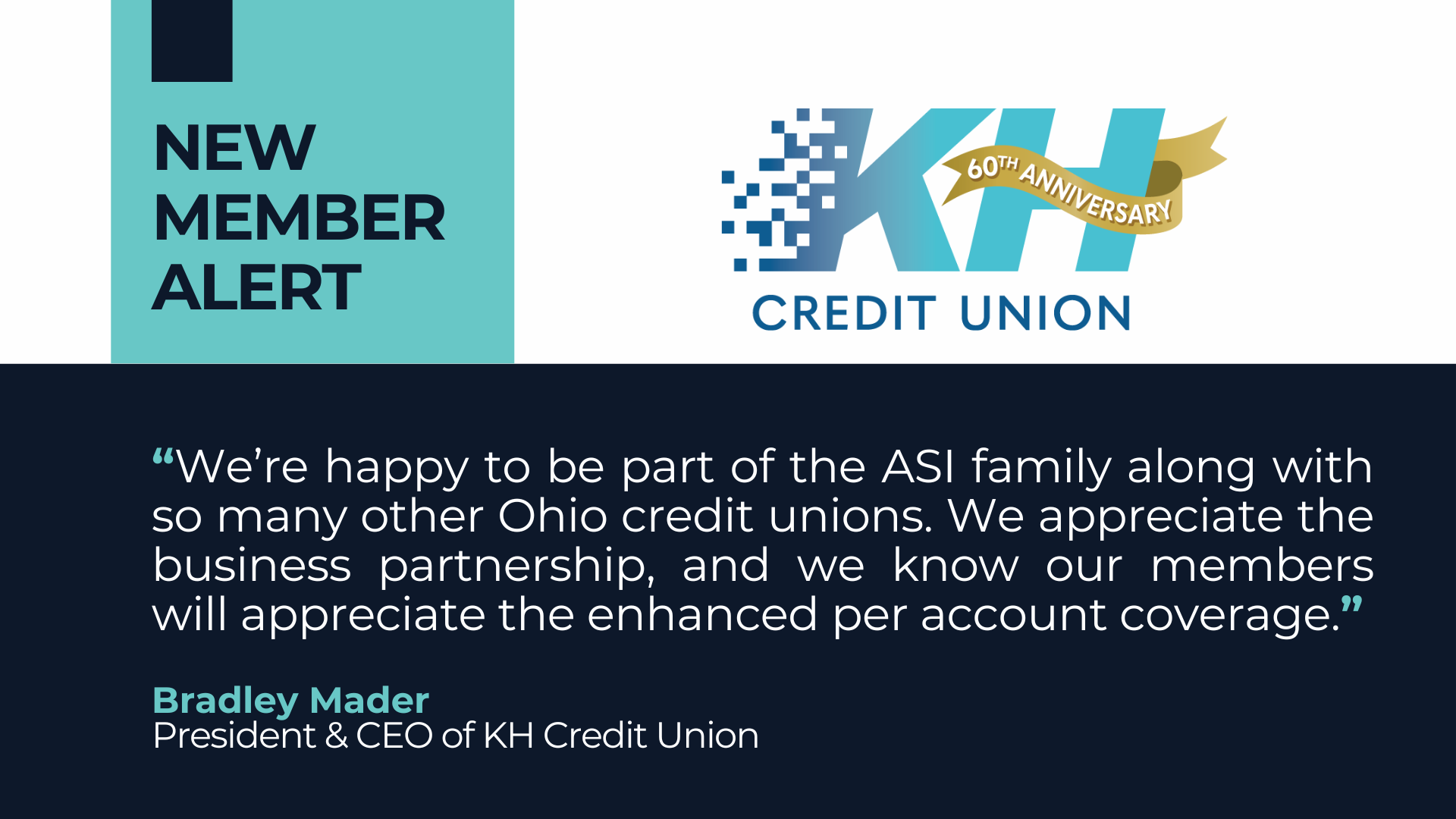

KH Credit Union converts to private share insurance through ASI

We are excited to announce that KH Credit Union, a $70 million institution based in Dayton, OH, has converted from federal to private share insurance with American Share Insurance (ASI).

2024 Year-End Financial & Economic Outlook for Credit Unions

Watch our complimentary webinar to get valuable insights into the economic outlook for the coming year, specifically tailored to the needs and challenges facing credit unions.

American Share Celebrates 50 Years of Helping Credit Unions Succeed

For half a century now, ASI has been a pillar of support and innovation in the credit union industry, providing a strong private deposit insurance option that champions state sovereignty and strengthens the dual chartering system.

Authority Magazine Interview with President/CEO, Theresa Mason

President & CEO, Theresa Mason, has been featured in Authority Magazine. In her recent article, she takes us through her inspiring leadership journey, shedding light on the experiences and insights that have shaped her career.